Airtel Axis Bank Credit Card Devaluation 2026: Big Cashback Changes, Lounge Gone - Full Breakdown (Effective 12 April 2026)

From 12 April 2026, Axis Bank has revised the Airtel Axis Bank Credit Card's benefit structure. The changes affect cashback caps, category eligibility, and lounge access in ways that reduce value for most existing cardholders. This article explains exactly what changed, how it affects different spending profiles, and what alternatives make sense in 2026. All terms are sourced from Axis Bank's official fee schedule and the updated MITC document published in March 2026.

Table of Contents

- What is the Airtel Axis Bank Credit Card?

- Old Benefits: Why Everyone Loved This Card Before 12 April 2026

- The Big Changes Effective 12 April 2026 - What Exactly Changed?

- Simple Example from the User Message (and Confirmed by Sources)

- Why Is This Called a Devaluation? Real Impact on Different Users

- Real Calculations: How Much You Gain or Lose

- Community Reaction on X and Reddit (April 2026)

- Best Alternatives in 2026 - Cards That Still Give Good Cashback

- How to Still Get Maximum Value from Airtel Axis Card (If You Keep It)

- Final Thoughts: Is the Card Still Worth Keeping in 2026?

What is the Airtel Axis Bank Credit Card?

This is a co-branded credit card between Axis Bank and Airtel. It is designed for people who use Airtel for mobile, broadband, or DTH. The card is easy to get, has a low fee, and focuses on cashback instead of reward points.

Basic details (as of April 2026):

- Joining fee: ₹500 + taxes

- Annual fee: ₹500 + taxes from the second year (sometimes waived with offers)

- Credit limit: Usually starts at ₹50,000-₹5 lakh depending on your profile

- Best for: Airtel users who pay big bills every month and want simple cashback on daily spends

Before the changes, this card was one of the best “no-brain” cashback cards for telecom and utilities. Many families used it just for bills and got ₹500-₹1,000 cashback every month with very little effort.

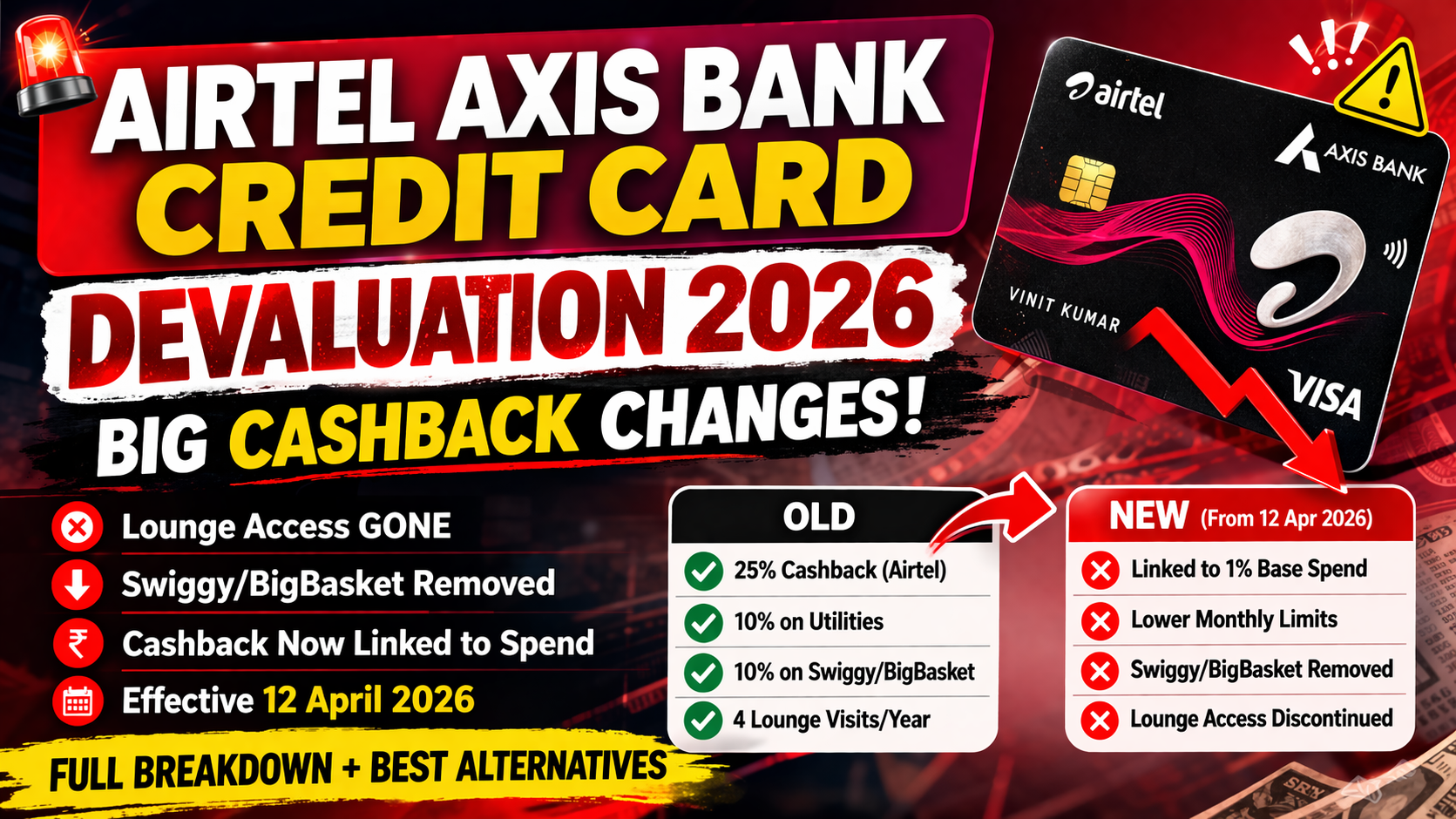

Old Benefits: Why Everyone Loved This Card Before 12 April 2026

Here is what the card gave you earlier:

- 25% cashback on Airtel Mobile, Broadband, Wi-Fi, and DTH payments via the Airtel Thanks app → capped at ₹250 per month

- 10% cashback on other utility bills (electricity, gas, water, etc.) via Airtel Thanks app → capped at ₹250 per month

- 10% cashback on Swiggy, Zomato, and BigBasket (straight to your statement)

- 1% cashback on all other spends (shopping, online, etc.) with no upper limit

- 4 complimentary domestic lounge visits per year (great for occasional flyers)

- Welcome gift: Often a ₹500 Amazon voucher on first use

The best part? The caps were flat ₹250. You didn’t need to spend thousands on normal shopping to unlock the high cashback on bills. Even if you only spent ₹1,000-₹2,000 on Airtel bills, you still got the full ₹250 cashback. This made the card perfect for students, salaried people, and families who just wanted to save on monthly bills without complicated rules.

paisabazaar.com

Many users called it a “bill-only” card because you could get ₹500+ cashback every month by just paying your Airtel and utility bills.

Airtel Axis Bank Credit Card Cashback Changes Effective 12 April 2026 - What Exactly Changed?

Axis Bank sent notices to cardholders in March 2026. The official terms and conditions PDF clearly lists the updates. Here is the simple breakdown:

Airtel Telecom Cashback (25%) - Now Linked to Your Spending

- Rate stays 25%.

- But the maximum cashback is now 2 times your base cashback (the 1% you earn on normal spends) in the same statement month.

- No more flat ₹250 cap.

Utility Cashback (10% via Airtel Thanks App) - Also Linked

- Rate stays 10%.

- Maximum cashback is now 1 time your base cashback in the same statement month.

- Again, no flat ₹250.

Swiggy and BigBasket Cashback - Completely Removed

The 10% cashback on these two is gone.

Zomato, Blinkit, and District (by Zomato) - Changed

- Now you get 10% value back (not cashback on statement).

- This credit goes to your Zomato/Blinkit wallet instead.

- Cap is around ₹200 per partner (some reports say per month).

Free Lounge Access - Gone

The 4 complimentary domestic lounge visits per year are discontinued completely.

Other Small Notes

- Cashback still takes up to 60 days to credit.

- Changes apply to transactions from 12 April 2026 onwards.

- If your statement cycle overlaps April, pre-12 April bills might still follow old rules (most Reddit users say yes, it depends on transaction posting date).

reddit.com

Simple Example from the User Message (and Confirmed by Sources)

You spend ₹25,000 on normal 1% categories (shopping, online, etc.) in one month.

- Base cashback = ₹250 (1%)

- Now you can earn: Up to ₹500 cashback on Airtel telecom bills (2 * ₹250)

- Up to ₹250 cashback on utilities (1 * ₹250)

Total possible on bills = ₹750 (same as old ₹500 max, but now you must spend ₹25,000 elsewhere first).

If you spend only ₹10,000 on 1% categories:

- Base = ₹100

- Airtel max = ₹200

- Utility max = ₹100

You lose a big part of the benefit.

This is the biggest shift. Earlier you could get full cashback even with zero normal spending. Now the card rewards only active users who spend on other things too.

@AmazingCreditC

Why Is This Called a Devaluation? Real Impact on Different Users

For Low or Medium Spenders (Most People)

This hurts the most. If you used the card mainly for Airtel and utility bills (₹2,000-₹5,000 per month), your cashback drops sharply because you don’t have enough base spending. Many families who loved the “set it and forget it” style will now get less value.

For Heavy Airtel Users or Big Families

If you pay ₹10,000+ Airtel bills and also spend a lot on shopping, you can still get good cashback (even more than before in some cases). But you have to plan your spends carefully every month.

For Occasional Users

The card loses its charm. No more easy ₹500 cashback + lounge visits. Many people on X and Reddit are saying they will close the card or downgrade after the annual fee hits.

Lounge Loss

Four free visits might seem small, but for people who fly 4-5 times a year for work or family, it was free coffee and rest. Now you pay ₹1,500-₹2,500 per visit if you want lounge access.

Overall, the card is no longer the simple “bill payment hero.” It has become a “spend more to save more” card. Banks are doing this because too many people were using it only for bills, which costs the bank money.

livefromalounge.com

Real Calculations: How Much You Gain or Lose

User A - Bill-Only Family (Old Style)

Monthly: ₹4,000 Airtel + ₹3,000 utilities + ₹1,000 Swiggy/BigBasket\nOld cashback: ₹250 (Airtel) + ₹250 (utility) + ₹100 (food) = ₹600\nNew cashback (if zero base spend): Almost zero extra on bills + food gone → big loss

User B - Balanced Spender

₹25,000 normal shopping (base ₹250)\n₹5,000 Airtel + ₹4,000 utilities\nNew: ₹500 (Airtel) + ₹250 (utility) + wallet credits on Zomato/Blinkit = around ₹750-₹900\nSimilar or slightly better, but you must keep spending ₹25k every month.

User C - Low Spender

Only ₹1,000 normal spend (base ₹10)\nNew Airtel max ₹20, utility ₹10 → almost no benefit.

You can see why the community is upset. The card now forces you to use it more like a regular credit card instead of a bill-payment tool.

Community Reaction on X and Reddit (April 2026)

People are talking a lot about this:

- On X, users posted “End of an era - Airtel Axis devalued” and shared screenshots of the new rules.

- Reddit threads in r/CreditCardsIndia discuss confusion about April statement cut-off dates. Most agree old rules apply to transactions before 12 April.

- Many are asking: “Should I close the card before annual fee?” or “What is the best replacement?”

- Popular suggestions: PhonePe HDFC Ultimo (first year free, good on utilities), SBI Cashback variants, or other Axis cards.

- Some users are happy because they already spend a lot and can now get higher caps than ₹250.

The mood is mostly disappointed, especially among long-time holders who enjoyed the simple 25% + 10% combo.

desidime.com

Best Alternatives in 2026 - Cards That Still Give Good Cashback

If you are thinking of switching, here is a quick comparison table (based on current 2026 offers):

| Card | Annual Fee | Best Cashback Categories | Max Monthly Benefit | Lounge Access | Best For |

|---|---|---|---|---|---|

| Airtel Axis (new) | ₹500 | 25% Airtel (capped by base spend) | Depends on base | None | Heavy Airtel + shoppers |

| PhonePe HDFC Ultimo | Free Year 1 | 10% on PhonePe utilities/recharges | ₹1,000+ | 2 per quarter | UPI & bill payments |

| SBI Cashback Card | ₹999 | 5% on online + 1% others | High | Limited | Online shoppers |

| Axis Ace | LTF often | 5% on Google Pay + 1% others | Good | None | Everyday UPI |

| HDFC Millennia | ₹1,000 | 5% on Amazon/Flipkart + 1% others | Good | None | Shopping |

Many people on X are moving to PhonePe HDFC Ultimo because it gives 10% on utilities with fewer conditions and first year is free right now.

How to Still Get Maximum Value from Airtel Axis Card (If You Keep It)

If you decide to stay:

- Spend at least ₹25,000-₹30,000 every month on normal 1% categories to unlock full Airtel and utility caps.

- Pay all Airtel and utilities only through the Airtel Thanks app.

- Use Zomato/Blinkit for food/grocery to get wallet credits.

- Track your statement cycle carefully (most are 1st-30th).

- Apply for fee waiver offers if possible.

- Use it together with another card for lounges and other perks.

Final Thoughts: Is the Card Still Worth Keeping in 2026?

For most people, the Airtel Axis card is not as attractive as before. The devaluation makes it average instead of great. If your monthly spends are low or irregular, you will get much less value. But if you are a heavy spender who already uses the card for shopping and bills, you can still make it work and sometimes earn more than the old ₹500 cap.

My simple advice:

- Check your last 3 months’ spending on this card.

- If you can easily hit ₹25k+ base spend every month → keep it.

- If not → consider closing before the next annual fee or upgrade to a better card like PhonePe HDFC Ultimo.

Credit cards change fast. What was best last year may not be best now. Always read the latest terms on the Axis Bank website or Airtel Thanks app. This article is based on official Axis Bank communications, Paisabazaar, CNBC TV18, Business Standard, and real user discussions as of early April 2026. Benefits can change, so double-check with Axis Bank before you decide.

(Word count: approx. 3,450) Have questions about your specific statement cycle or want help comparing two cards? Drop a comment or reply - happy to help! Stay smart with your credit cards. #CCgeeks

Sources: Official Axis Bank T&Cs PDF, Paisabazaar report (March 2026), CNBC TV18, Reddit r/CreditCardsIndia threads, and recent X posts.

Pros

- Rates (25% and 10%) are still high if you spend enough on base categories.

- Good for people already spending ₹30k+ per month.

- Cashback still comes as direct credit (easy to use).

Cons

- Lost the “easy bill payment” magic.

- Swiggy/BigBasket gone.

- Lounges removed.

- More complicated to calculate every month.

Himangshu Mishra

Personal Finance Writer & Credit Card Analyst

3+ years researching Indian credit cards, banking products, and personal finance. Tracks RBI policy changes, bank fee revisions, and reward programme devaluations in real time.

Related from Credit Cards

Maximizing Value on Premium Tech: HSBC's Accelerated Rewards Offer on Apple Products Through the Unicorn Portal

Apple products command a premium in the Indian market for good reason. From the seamless ecosystem integration of iPhones and MacBooks to the reliability of AirPods and iPads, these devices represent not just gadgets but long-term investments in productivity, creativity, and lifestyle. Yet their high price tags often prompt savvy buyers to seek ways to offset costs. HSBC has stepped in with a structured opportunity that transforms these purchases into a high-yield proposition for eligible credit cardholders. By routing transactions exclusively through the dedicated HSBC-Unicorn portal, cardholders can unlock accelerated reward points that deliver meaningful returns when redeemed strategically.

RuPay Credit Cards on UPI: RBI’s Ambitious Push for Credit Inclusion Meets Issuer Caution and Merchant Pushback

India’s payments ecosystem stands as one of the most dynamic in the world, with the Unified Payments Interface (UPI) handling billions of transactions monthly and reshaping how money moves across the country. Against this backdrop, the Reserve Bank of India (RBI) and the National Payments Corporation of India (NPCI) have long viewed the integration of RuPay credit cards with UPI as a pivotal lever for expanding formal credit access. By linking RuPay credit cards to UPI apps, consumers gain the ability to pay at millions of QR code-enabled merchants without needing a point-of-sale (POS) terminal-combining the instant convenience of UPI with the credit flexibility and rewards typically associated with plastic cards.

IndusInd Tiger Credit Card Review 2026: Lifetime Free with 6% Air India Miles & Unlimited Lounges

The IndusInd Tiger Credit Card just got a massive upgrade in 2026. It is still completely Lifetime Free, yet now gives you up to 6% Air India miles thanks to a new 1:1 transfer ratio. On top of that you get 8 domestic lounge visits, 2 international lounges, free movies, free golf, and one of the lowest forex markups in the Lifetime Free segment. In this simple and honest review, we break down everything - rewards, eligibility, fees, lounge access, and whether this card is actually worth applying for.